The GST Group of Ministers (GoM) has put forward a recommendation to completely exempt health and life insurance premiums from GST. If the GST Council adopts it, this move would reduce insurance costs for millions of Indians. Experts, however, caution that customers would undoubtedly get relief in post-tax premiums but that the overall effect would depend on the implementation of the exemption, especially on Input Tax Credit (ITC). This is especially important for understanding the GST Exemption for Health and its implications, which can lead to a significant improvement in the healthcare sector.GST Exemption for Health has been a topic of discussion among policymakers and stakeholders.

Present GST Burden on Insurance Premium and the GST Exemption for Health

Currently, life insurance and health insurance premiums both charge an 18% GST, directly contributing to increasing the policy cost. For example, a ₹100 life insurance policy turns into ₹118 after charging GST.

But Insurers have the benefit of Input Tax Credit. Since they pay GST for office lease, brokerage to agents, and advertisement expenses, they can set this tax off against GST collected from policyholders. For instance, when an insurer collects ₹18 as GST from customers, it is able to reduce this expense by claiming credit for taxes already paid on expenses, thereby decreasing its net GST obligation. This step limits insurers’ tax bills, though the customer has to pay higher.

What happens if GST is scrapped?

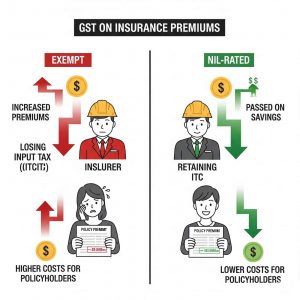

When GST on insurance premiums is scrapped altogether, the impact would be based on whether or not such services are “exempt” or “nil-rated” or not.

Exempt Classification: Insurers will not be able to recover ITC on their expenses in such a situation. This will render GST paid on rent, marketing, and commissions an added expense. In order to negate profitability, insurers will be able to increase the base premium, reducing the benefit of the policyholder.

Nil-Rated Classification: In case policies are announced nil-rated, insurers will continue to benefit from ITC. This will help them pass on the complete benefit of tax savings to customers, leading to a certain reduction in post-tax premiums.

Thus, the real advantage to policyholders depends upon the exemption as articulated by the GST Council.

Expert Views on the Proposal

According to Pankaj Goel, Partner at CNK, this is a forward-looking measure that could make insurance more affordable and bolster social security. He says the exemption on premium payment will make health and life covers affordable to more people, especially the middle class, while gently elevating disposable income.

Alok Rungta, MD & CEO, Generali Central Life Insurance, explains the impact through an example: “At a premium of ₹100, customers are now paying ₹118 after GST. With exemption, the tax component reduces to zero, and benefits can be passed through in full. Customers will obviously see a reduction in payable amount.”

Hemik Shah, Co-Founder at Qian Insurance, warns that the benefit is entirely at the mercy of classification. If policies are exempted, ITC would not qualify, and premiums could increase. But if they are nil-rated, credits would remain eligible, and insurers can transfer benefits to customers.

Anandaday Misshra, Founder, AMLEGALS, notes that total exemption could ironically drive up the cost to insurers due to the forgone ITC. He emphasizes that regulator oversight is required so that the relief actually trickles down to policyholders.

Sudipta Sengupta, CEO, The Healthy Indian Project, adds that unless ITC is brought back, insurers would have to raise premiums to take in non-recoverable costs, thus diluting the relief desired.

On the other hand, Ayush Patodia, AVP, Avalon Consulting, considers the move as an opportunity for insurance firms to get lean. According to him, phasing out ITC will compel firms to streamline wasteful marketing expenditures, embrace digital enablers like e-KYC and telemedicine, and expand reach through microinsurance and rural partnerships.

Balancing Consumer Relief and Industry Viability

The proposal is also geared to enhance insurance penetration in India, where coverage levels are woefully low. Lowering the upfront tax burden may encourage individuals to buy health and life insurance policies. But in the absence of proper classification and ITC transparency, the exemption may end up raising insurers’ costs and forcing them to hike premiums.

Conclusion

The proposal to exempt life and health insurance premium from GST is a pro-reform change in India’s fiscal landscape. If it is prescribed as nil-rated, it can go a long way in streamlining policy costs, increasing affordability, and supporting the government’s overall goal of strengthening social security. But if it is interpreted as exempt, insurers may actually absorb some extra operational costs, which could reduce the benefit for policyholders.